Monday Market Review: June 15, 2026

- Investment Committee

- 14 minutes ago

- 7 min read

Weekly Summary

Economic data included rises in consumer and producer prices, which were expected, but still not necessarily celebrated. Though, existing home sales and consumer confidence showed some improvement.

Equities saw positive results around the world, with renewed hopes for a U.S.-Iran deal and progress towards a Strait of Hormuz reopening. Bonds also rose with inflation-related yields coming back down a bit. Commodities weakened on the back of oil prices normalizing downward, due to the same Middle East expectations.

What to know about the markets:

U.S. stocks were mixed by mid-week as U.S.-Iran rhetoric having ramped up again, as well as inflation reports reminding investors about the price impact of continued tensions, but improved with hopes of a completed peace deal, threatened military strikes from the U.S. that were walked back, and continued tech optimism. (A deal being reached over the weekend has pushed stock futures up and oil prices down so far this morning.)

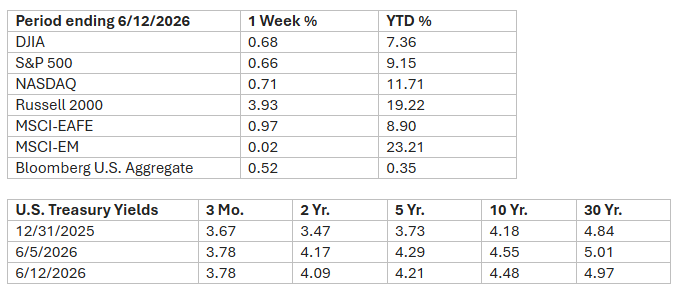

Nearly every sector ended in the positive last week, aside from a drop of a few percent in communications and slight decline in energy. Leaders included the eclectic mix of materials (copper mining), consumer staples, and financials. Real estate also gained over a percent for the week. Small cap stocks outperformed large caps by several percent, in keeping with greater risk-taking by investors. The largest-ever IPO for SpaceX was the primary single-stock news of the week, with the $135 IPO price moving to an opening price of $150, with Friday trading showing a 20% spike. As under 5% of the total company was floated in the IPO, it implied a near-$2 tril. market value.

Foreign stocks performed largely in line with the U.S. last week, with hopes for a Strait of Hormuz opening boosting sentiment along with potential oil flows. The ECB raised interest rates by 0.25% last week, the first major central bank to hike, calling the move “obvious and sensible” considering inflation running over 3% and expecting to run above target for much of the next year. However, questions from other observers focus on the potential demand destruction from high oil prices on economic growth, which could ultimately justify the opposite response (and what the ECB has ultimately done in several of the last few cycles). It’s possible the Bank of Japan will hike as well, although trying to stabilize a weaker yen is a larger consideration there. Emerging markets were mixed, with returns country-specific, and showing no clear pattern.

Bonds fared positively around the world, as interest rates broadly fell—this was in line with hopes for eased future inflation that offset the more negative U.S. CPI and PPI reports that showed strong negative impacts from the oil price spike in recent months. Investment-grade and high yield outperformed governments slightly, while emerging market debt benefitted from positive risk-taking sentiment for the week.

Commodities pulled back as a whole, due to energy prices falling back, followed by weakness in precious metals. West Texas crude oil and Brent crude prices each declined by -7% last week to $84/barrel and $87/barrel, respectively, along with the broader theme of hopes of a Middle East peace deal.

Our Weekly Economic Notes:

Notes key: (+) positive/encouraging development, (0) neutral/inconclusive/no net effect, (-) negative/discouraging development.

(-) The Consumer Price Index for May rose by 0.5% on a headline level, quite high but also on par with expectations. That was led by energy prices rising by 4% in the month (7% for gasoline), continuing several months of extreme gains. Core CPI, ex-food and energy, rose 0.2%, which annualizes to a much more normal pace. Per the BLS, important rising indexes included communication (1.3%, mostly due to wireless phone services), airline fares (2.7%), personal care (1.0%), medical care, and recreation. On the other hand, declines were seen in car insurance (-1.7%), prescription drugs (-0.9%), household furnishings/operations (-0.6%), and new cars/trucks.

On a year-over-year basis, headline CPI rose 4.2%, and core up 2.9%. These were obviously both elevated well above normal, due to energy commodity prices up 41%, but food was up 3%, and shelter in the mid-3’s, each far lower in comparison despite above target. The pared-down core measure of “All items less food, shelter, and energy” rose a mere 2.4% for the past year, which bordered on normal. Also on the positive side, core goods inflation has seen some improvement after having last year’s tariff impacts beginning to roll off. Financial markets are never thrilled about inflation readings this high, but have tolerated them a bit better when an end seems to be in sight. Early in the U.S.-Iran conflict, the timeline was assumed to be short, but the longer until a potential resolution drags on, the less accommodating is the patience of the world’s investors.

(-) The Producer Price Index for May rose by 1.1%, the same as the prior month, but exceeded the 0.7% expected. As with CPI, energy led the way, up 11%. Removing food and energy, core PPI rose 0.4%, which was still high when annualized. Goods prices overall rising nearly 3% was the largest single-month increase in the history of that series going back 17 years, and represented nearly all of the monthly increase. Perhaps less-known is the impact on the services side of portfolio management fees, which have risen along with the rise in the stock market, and point to the interconnected and nuanced nature of some of this data. Year-over-year, headline PPI rose 6.5%, with core up 4.9%. The full year period was high on both fronts, with goods prices over 10% (final demand energy up 37%, along with strong gains for metals and electronic components) and services up 5%.

(+) Existing home sales rose 3.2% in May to a seasonally-adjusted annualized pace of 4.17 mil. units, above the 1.1% gain expected, in addition to an upward revision for April. For May, the gains were led by single-family, up over 3%, while condos/co-ops were little-changed. Regionally, the largest increases were seen in the Midwest (6%), while those in the West were unchanged. Nationally sales were up 3% over the past year. The median existing home sales price rose 2.8% for the month to $429,300, which only represented a 1.3% increase year-over-year. Inventories came in at 4.5 months’ supply, which remains below the level considered to be a ‘normal’ market. Affordability remains a problem, with higher long-term U.S. Treasury yields leading to elevated mortgage rates, although the slower pace of home price appreciation is now below that of wage growth, which is a positive on the affordability side for a change.

(0) The preliminary Univ. of Michigan index of consumer sentiment for June showed a rise of 4.1 points to 48.9 (or 9.2%), beyond the median forecast of 46.0. Assessments of current economic conditions rose by nearly 6%, while expectations for the future rose by 12%. Year-over-year, the overall index remains down -19%, with current conditions being the key driver, down -25%. Inflation expectations for the coming 1 year fell by -0.2% to 4.6%, while those for the coming 5-10 years fell by -0.5% to 3.4%. Anecdotal commentary noted that consumers felt “some relief” due to an easing in gasoline prices early in the month, particularly in the lower-income cohort that’s most sensitive, as “gasoline comprises a larger share of their budgets.” Overall, consumers continue to “feel burdened” by the recent higher inflation readings and “worry that higher inflation could remain stubborn going forward, particularly in the short run,” and that “views of the economy are still relatively dour.” There were no surprises here, but the pattern echoes financial markets, that continue to see the Middle East conflict as a limited-term speed bump, as opposed to long-term.

(0/-) Initial jobless claims for the Jun. 6 ending week rose by 4k to 229k, just above the 220k median forecast. Continuing claims for the May 30 week rose by 24k to 1.795 mil., above the 1.785 mil. expected. It’s been mentioned that the Memorial Day weekend could have created some seasonal adjustment challenges, but otherwise claims have stayed within a fairly limited band and don’t point to an eroding labor market.

Have a good week.

Have investment questions? We're here to help. Schedule a call a complimentary Basics of Investing Zoom Session here.

Centered Financial, LLC is a registered investment adviser offering advisory services in the State of California, Utah, Texas and in other jurisdictions where exempted. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. There is no assurance that the techniques, strategies, or investments discussed are suitable for all investors or will yield positive outcomes. To determine which strategies or investment(s) may be appropriate for you, consult your financial adviser prior to investing. Any discussion of strategies related to tax or legal planning is general and is not intended as tax or legal advice. Please consult appropriate tax and legal professionals for recommendations pertaining to your specific situation.

Sources: Ryan M. Long, CFA; Director of Investments; Palouse Capital Management

Palouse Capital Management, American Association for Individual Investors (AAII), Associated Press, Barclays Capital, Bloomberg, Citigroup, Deutsche Bank, FactSet, Financial Times, First Trust, Goldman Sachs, Invesco, JPMorgan Asset Management, Marketfield Asset Management, Morgan Stanley, MSCI, Morningstar, Northern Trust, PIMCO, Standard & Poor’s, StockCharts.com, The Conference Board, Thomson Reuters, T. Rowe Price, Univ. of Michigan, U.S. Bureau of Economic Analysis, U.S. Federal Reserve, Wall Street Journal, The Washington Post. Index performance is shown as total return, which includes dividends. Performance for the MSCI-EAFE and MSCI-EM indexes is quoted in U.S. Dollar investor terms.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product. Advisory Solutions Group is a registered investment advisor.

Comments